{kind=link}

{kind=link}

The RDR (Retail Distribution Review) process is driving a number of regulatory reforms that are impacting revenue streams, governance processes, data exchange and system integration requirements. Against this background of increased regulation and greater compliance costs, Andrew Coutts, head of intermediated distribution at Santam, shared his thoughts on the opportunities this brings for intermediaries and insurers to evolve their businesses for the better.

What is the intent of these regulations?

The new amendments are intended to increase policyholder protection and lessen the risk of biased advice by introducing a number of processes relating to product governance, channel oversight, claims management and complaints management. It’s all about fair customer outcomes: it’s the right thing to be doing and should be part of core business practice, but ensuring effective implementation and good change management will require business focus and priority.

It does present an opportunity to improve businesses, create more professionalism and to showcase the value of advice. What’s more, there is a need for better disclosure and governance from insurance companies.

Why were regulations necessary?

The Regulator was concerned that there wasn’t always an equivalence of fee-for-activity in the market and that not all activities in the insurance value chain were always being performed in the best interest of the customer. With an ever-increasing demand for transparency and an increasingly informed and demanding customer, regulators saw it necessary to ensure a greater degree of alignment, to drive technology integration of sources and improve disclosure.

We’ve engaged extensively with the regulators in making sure that we get that intervention right. The challenge we had to address was the competing requirements of managing efficiency while ensuring we did not ignore complexity or stifle innovation.

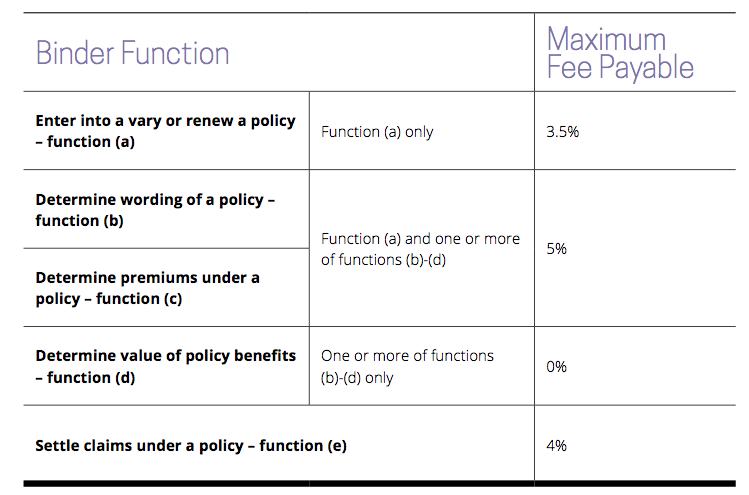

Understanding the 9% cap on remuneration

The 9% capped binder fee decision was the outcome of detailed engagement between two leading industry bodies: the Financial Intermediaries Association (FIA) and the South African Insurance Association (SAIA). The amended regulations stipulate that binder holders – authorised to give advice under the Financial Advisory and Intermediary Services (Fais) Act – may receive a maximum of 9% in remuneration for binder activities as defined. The fees and activities are broken down into three sub-categories:

- A 3.5% fee is payable for entering into, varying or renewing policies on behalf of the insurer.

- You can earn a further 1.5% fee (a total of 5%) if you determine policy wording, policy premiums or policy benefits. Where you perform these functions for an insurer, you accept responsibility for sustainably managing rating customer segmentation and policy summary on behalf of the insurer.

Remuneration must:

- Be reasonable and commensurate with the function or activity performed.

- Not result in remuneration being paid a second time for a function or activity for which commission or a binder fee is paid.

- Be fair to policyholders.

- Not be linked to claims rejected wholly or partly.

An opportunity to do better business

Customers don’t always know what they get when they deal with an intermediary so an opportunity exists to showcase why it is so much better to do business with a broker. In a world of so much complexity and change, is a customer really enough of an expert to properly insure themselves, or is there real value in getting a professional to give you advice?

Intermediaries must embrace the opportunity to move up in the complexity value chain and to do business in the lower value market differently. We hear a lot of talk about technology, on-demand platforms and robotics, but remember that these tools are equally available to you as an intermediary.

Do business differently and you can still be very successful in the commodity end of the market. Retain more hands-on and more face to face business relationships only where the value of the commission and fee earnings allow you to do that. You can expand your offering, be more flexible and be relevant no matter where you are in the price point.

Technology doesn’t replace us, it augments us

The way brokers interact in future will certainly change. Some brokers will lead that change while others might choose to retain their status quo. Fundamentally there is so much opportunity to evolve. Technology allows us to do things differently. Digital platforms, in particular, fundamentally expand reach, allow for rich, low cost customer engagement and enable efficiency through customer self-help.

Explaining fees and justifying the service and value added

The real value for a broker in a Santam context is the incremental ability to know your customer and know your customer’s needs. This fundamentally starts with a good approach to needs analysis. Use that opportunity to explain and manage the expectation of your client to really know the risk that you’re insuring and make sure the customer also knows the risk that they are not insuring, and to explain and validate what you are offering as a service.

If there is complete transparency upfront and expectations are clear, the ability to deliver on the value proposition of insurance - putting you back in the position you were should a claim happen - will not be a problem. Therefore, engage, take the time to understand the problems upfront and you won’t have a problem at the end.

How insurers will oversee binder agreements

The new regulations state that “the insurer is the overseer of the conduct of binder agreements and is accountable to the registrar for the failure of their binder holder as to performance and integrity”. There is an onus that comes with the new regulation and a large part of it is around the governance and control processes. The impact on Santam is that there will be much more focus on our due diligence processes and how we select our binder partners. We will naturally end up with significantly less partners over time. As a binder holder you can expect more intrusive behaviour from your insurer because they have to get more involved in how you deliver these services to your clients.

Expect routine quality assurance audits and an increased demand for data. You can expect far more active interaction around policy screenings, new client vetting, management of sophisticated rating models around segmentation, pre-screening, optimisation of new business, leads, quotes, lifetime value segmentation and renewals. All those typical pricing engines that sit at the back of insurance are now laid forward into binder holders because of better integration of data.

While it may feel like more work and effort, the improved efficiency and rigour have huge benefits in sustaining the outcome - both in terms of value to the client but also in terms of the profitability and sustainability of the binder holder and the insurer.

Santam stands behind its intermediaries

Customers need good advice now more than ever which is why Santam continues to believe strongly in the value and power of intermediaries. It is by far our channel of choice and continues to be the largest distribution channel in the world.

It is important to recognise that regulations are not going to go away and it’s best to not fight it but deal with it. Find a way to utilise the investment and the cost to improve the value proposition of what you offer to your clients and grow your professionalism. See training requirements as an opportunity to grow you skills and change the offering of what you’re providing, and use it to potentially justify higher advice fees. Leverage the ability to generate new revenue streams by doing things better and more professionally.

The real value of outsourcing has been to link the client to the insurer, and leveraging the power of intermediaries to make decisions on behalf of insurers. Integration of data that is now a requirement and the closer controls will result in more accuracy, better pricing and a more sustainable outcome. It’s our challenge to make it work for customers and to adapt to change.

Remember you don’t have to do everything yourself

There are lots of people out there who can help you adapt to technology and regulations. Partnering with them is an important way of surviving changes. At Santam, we want you to be successful and we are very committed walking this journey with you and to giving you every possible support through these challenging times.

By leveraging new technologies, creating partnerships, and leaning on each other, we can create new revenue streams, add efficiencies and improve our collective customer value propositions. By effectively embracing and managing change, it is possible for us to use the change as a springboard for great success in future.

If you’d like to know more about the new regulations and relevant training for yourself and your staff, please contact us. For more advice tailored to intermediaries, visit our blog where you will find more useful articles, such as how you can add value to your customers far beyond a good price.